Over the last few months you may have been surprised to see the HNI portion of some of the IPOs being oversubscribed by 300 and 500 times. If you are wondering what is driving this kind of oversubscription, then it is the power of IPO funding. Many banks and finance companies provide loans to HNI investors to apply for IPOs. The business of IPO funding is fairly safe as it is secured by the shares allotted in the IPO. But the bigger question is whether IPO fund makes economic sense for the investor. Do investors really make money on an IPO after considering the interest cost of IPO funding? But first a primer on the IPO application categories!

There are 3 classes of investors that are provided for in the IPO application. Firstly, there is a quota for the qualified institutional buyers (QIBs). These are institutional buyers like mutual funds, foreign portfolio investors, insurance companies, banks, sovereign funds etc. The second category is the Retail category wherein small investors up to an investment of Rs.2 lakh per IPO are accepted. The last category is the HNI or non-institutional category. This category includes wealthy individuals who are applying for shares worth more than Rs.2 lakhs in the IPO and other corporate investors, trusts and NBFCs that are not currently classified as institutions. It is this HNI category that goes for IPO funding. The allotment method for HNIs is proportionate allotment and hence funding becomes simpler and more predictable.

IPO funding may be for a very short period but the success of the IPO funding for an investor will predicate on a variety of factors. There are 5 key factors that will make funding attractive for the IPO investors in the HNI category…

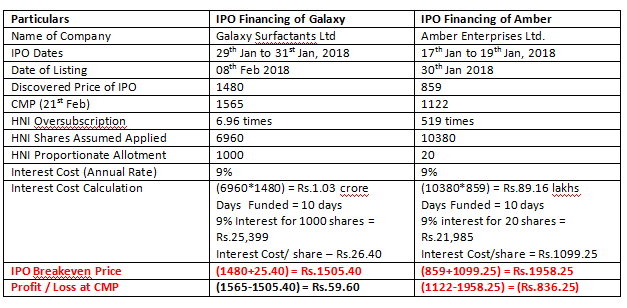

Let us understand the entire issue of IPO funding profitability with the example of two distinct IPOs that closed recently. Look how the extent of oversubscription completely changes the economics of a funded IPO.

In the case of Galaxy Surfactants the oversubscription of the HNI portion was just 6.96 times hence the cost of funding is just about adding 1.7% to the cost of the IPO. In such cases, even a nominal listing for the IPO will mean that the funded IPO will be profitable for the investor.

In the case of Amber Enterprises, however, the entire situation changes because the issue is oversubscribed 519 times. As a result the funding cost actually adds 128% to the cost of the IPO. Although the stock of Amber Enterprises listed at a premium of nearly 50%, that was not sufficient to make profits as the breakeven price is as high as Rs.1958.25.

The bottom-line is that in a funded IPO there is a major dilemma between the interests of the financer and the borrower. The financer will be most interested in funding the IPO only in case of heavy oversubscription whereas the investor will make money in a funded IPO if the oversubscription is nominal. It is between these two extremes that the IPO funding business operates.

Published on: Feb 26, 2018, 12:00 AM IST

We're Live on WhatsApp! Join our channel for market insights & updates

Get the link to download the App