The Fineotex Group includes Fineotex Chemical Limited (FCL), established as a public limited company in 2004. FCL, listed on both the Bombay Stock Exchange (since March 2011) and the National Stock Exchange (since January 2015), is a key player in the speciality chemicals and enzymes manufacturing sector, offering a wide range of products for various industries across 70 countries. Presently, Sanjay Tibrewala oversees day-to-day operations, while Surendra focuses on strategic decisions. FCL operates three manufacturing facilities in Navi Mumbai, Selangor (Malaysia), and Ambernath.

Over the past three years, Fineotex Chemical Limited (FCL) has demonstrated impressive financial performance, with a compounded sales growth rate of 38%. Notably, the company’s profits have surged with a compounded growth rate of 64%, reflecting its operational efficiency. FCL’s stock price has exhibited remarkable growth, with a CAGR of 111%, indicating investor confidence. Furthermore, the company’s robust return on equity, averaging 25% over the same period, underscores its ability to generate strong returns for shareholders. These financial metrics depict FCL’s promising growth trajectory and financial strength.

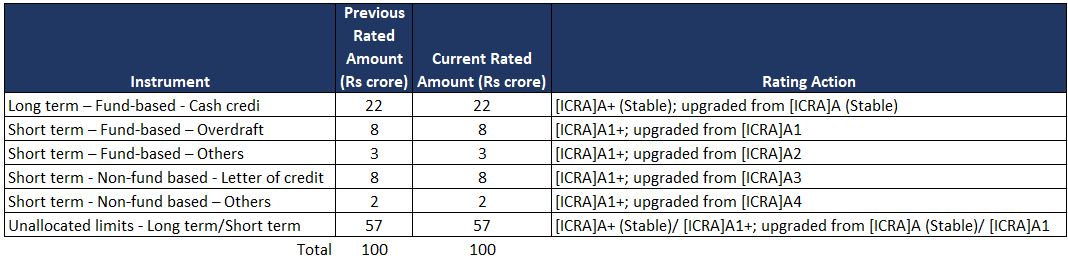

According to ICRA, Fineotex Chemical Limited (FCL) demonstrates substantial credit strengths.

According to the ICRA report, Fineotex Chemical Limited (FCL) faces significant credit challenges. ICRA has highlighted the following challenges for the company:

These challenges, as outlined by ICRA, underscore the importance of FCL’s strategies in order to sustain competitiveness and effectively manage the inherent risks associated with raw material costs and foreign exchange rate fluctuations.

Disclaimer: This blog has been written exclusively for educational purposes. The securities mentioned are only examples and not recommendations. It is based on several secondary sources on the internet and is subject to changes. Please consult an expert before making related decisions.

Published on: Nov 3, 2023, 11:53 AM IST

We're Live on WhatsApp! Join our channel for market insights & updates

Get the link to download the App