Small Finance Banks have emerged as a significant force within the Indian banking sector, catering to the financial needs of millions of customers who often remain underserved by traditional banks. These banks, with their primary mission to promote financial inclusion, bring banking services to the unbanked and underbanked sections of society. By analysing their Q2 results, we gain a clearer perspective on the state of these institutions, their impact on financial inclusion, and the challenges they face in a rapidly changing world.

In the second quarter of 2023, Small Finance Banks in India exhibited a diverse array of financial performances, shedding light on their resilience and adaptability in the ever-evolving financial landscape. Let’s delve into a comprehensive review of the Q2 results of prominent Small Finance Banks to gain a better understanding of how they fared.

| AU Small Finance | Ujjivan Small Finance | Equitas Small Finance | |

|

Sept’23 (Rs. Crore) |

|||

| Revenue | 2,531 | 1,391 | 1,359 |

| Financing Profit | 108 | 248 | 86 |

| Financing Margin % | 4% | 18% | 6% |

| Other Income | 425 | 189 | 181 |

| Net Profit | 402 | 328 | 198 |

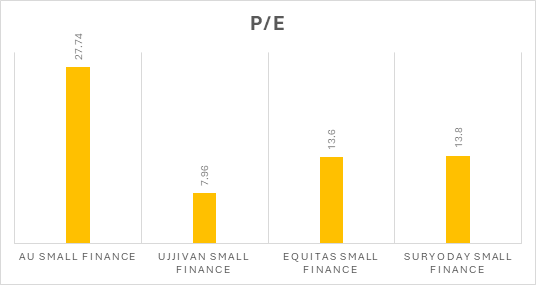

| EPS in Rs | 6.02 | 1.68 | 1.77 |

| Gross NPA % | 1.91% | 2.35% | 2.27% |

| Net NPA % | 0.60% | 0.09% | 0.97% |

Profit Growth

AU Small Finance Bank reported a robust performance in Q2FY24 with a net profit of Rs 401.8 crore, marking a 17.3% increase from the previous year. This reflects the bank’s capacity to deliver improved earnings.

Steady Net Interest Income

The bank’s net interest income (NII) for the quarter was Rs 1,249 crore, a 15.3% rise from the previous year, showcasing its ability to generate income from lending and borrowing activities.

Asset Quality Improvements

AU Small Finance Bank exhibited improved asset quality as its gross non-performing asset (NPA) ratio decreased to 1.76% in Q2FY24. However, the net NPA ratio saw a slight increase to 0.60% compared to the previous quarter.

Deposit Growth and Digital Expansion

The bank’s total deposits crossed Rs 75,000 crore, with a 30% annual growth. Moreover, the acquisition of 3.65 lakh new customers in the quarter, with 45% onboarded through digital channels, highlights the bank’s digital product success and expanding customer base.

Impressive Profit Growth

Equitas Small Finance Bank reported remarkable growth in Q2FY24, with a net profit of Rs 198 crore, marking a substantial 70.2% increase from the previous year. This reflects the bank’s robust financial performance.

Healthy Net Interest Income (NII)

The bank’s net interest income (NII) for the quarter reached Rs 765.6 crore, demonstrating a healthy 25% growth from the year-ago period. This showcases the bank’s ability to generate income from its interest-earning activities.

Notable Total Income Surge

Equitas SFB’s total income in the quarter surged to Rs 1,540.36 crore, a significant rise from Rs 1,147.39 crore in the corresponding quarter of the previous year, highlighting its strong financial momentum.

Growth in Credit and Deposits

The bank sustained credit growth, with advances increasing by 37% year-on-year and 6% quarter-on-quarter. Deposits also witnessed substantial growth, expanding by 42% year-on-year and 11% quarter-on-quarter to reach Rs 30,839 crore. Additionally, disbursements grew by 29% year-on-year to Rs 4,961 crore during the quarter, underlining the bank’s dynamic performance.

Profit Growth

Ujjivan Small Finance Bank reported a notable 11% increase in net profit for the second quarter ending on September 30, reaching Rs 328 crore. This growth was attributed to improvements in the bank’s asset quality, marking a promising financial performance.

Total Income Surge

The bank’s total income in the September quarter witnessed a significant increase, reaching Rs 1,580 crore, compared to Rs 1,140 crore a year ago. This surge reflects the bank’s ability to generate higher revenue.

Enhanced Asset Quality

Ujjivan Small Finance Bank’s asset quality improved, with a decline in gross non-performing assets (NPAs) to 2.35% of gross advances, compared to 5.06% in September 2022. However, net NPAs marginally increased to 0.09% from 0.04%.

Capital Adequacy Ratio (CAR)

The bank’s Capital Adequacy Ratio declined to 25.19% in this quarter from 26.70% at the end of the same quarter in the previous fiscal year, indicating potential implications for its future financial strategies and stability.

In summary, the fiscal period ending in September 2023 exhibited strong financial performance, with notable growth in net income and earnings per share, reflecting the company’s financial stability and resilience.

Disclaimer: This blog has been written exclusively for educational purposes. The securities mentioned are only examples and not recommendations. It is based on several secondary sources on the internet and is subject to changes. Please consult an expert before making related decisions.

Published on: Oct 30, 2023, 6:19 PM IST

We're Live on WhatsApp! Join our channel for market insights & updates

Get the link to download the App