Over the last three years the average Systematic Investment Plan (SIP) collections per month has almost doubled. During the year 2017-2018, SIP contribution accounted for around Rs 67,000 crore and the total number of active SIPs accounts stood at 2.52 crore. That is a huge number. But what exactly is a SIP? A SIP is a regular investment of a fixed amount into mutual funds (typically equity funds) each month.

For example, instead of investing Rs 1,20,000 in lump sum, you invest Rs 10,000 per month for the full year. What is the advantage of doing a SIP? There are three distinct advantages. Firstly, the SIP is a monthly commitment so it instills an element of discipline into your investment process. Secondly, your SIP outflows match with your income flows and thus you don’t have to worry about arranging the cash in one go. Last, but not the least, the SIP is instrumental in giving the investor the benefit of rupee cost averaging. By spreading your investment points across a period of time, the average cost of investing reduces as it makes the best of market volatility.

The only problem with the traditional SIP is that it assumes a constant SIP each month for a long period of time. But your incomes don’t remain constant over time. Normally, they increase over a period of time as all of us would have experienced with our income levels. If you are in a job then you get annual increments and if you are in business your revenues and profits grow over time. Higher incomes will automatically mean that you also increase your investments in sync with your growing income. Hence it would not be practical to assume the same amount of SIP for all these years. The answer to this challenge comes from the step-up SIP.

In a step-up SIP, you set a rule to automatically increase your monthly SIP contributions. In short, if you have a 20 year SIP, then you can hike the SIP amount every year or ever two years as you may be comfortable. This is perfectly in sync with your rising income levels. The most popular way of stepping up the SIP is on an annual basis. Broadly there are two approaches to stepping up your SIP; we are talking here about the rules for stepping up. The SIP can be stepped up on fixed rupee basis each year. For example you can start a SIP of Rs 5,000 per month and then step it up by Rs 1,000 every year. That means; over the next five years the monthly SIP contribution will be Rs 5,000 / Rs 6,000 / Rs 7,000 and so on. Alternatively, you can also step up your SIP on a percentage basis. In this case, you can start a SIP of Rs 5,000 per month and then step up by 10% each year. So over the next five years the monthly stepped-up SIP contribution will be Rs 5,000, Rs 5,500, Rs 6,050 and so on. The fixed monthly escalation is normally preferred as it is simpler to execute.

SIP is all about synchronising your investments with your income levels. The step-up SIP makes it an automatic and rule-based process. Normally, individuals tend to spend their incremental income and then realise that despite higher incomes, they did not save enough. A stepped-up SIP will avoid you this awkwardness by making higher savings a rule-based approach.

The step-up is determined in a way that your marginal propensity to save is increasing. That is one of the keys to wealth creation in the long run.

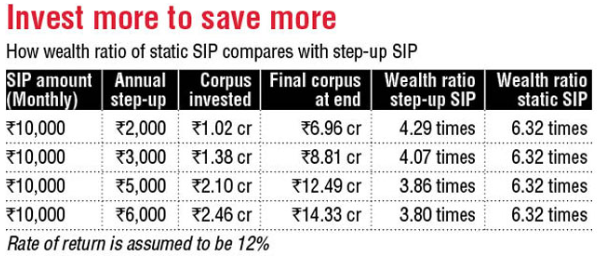

When you invest more money for a longer period of time you are likely to create more wealth. But you really need to look at the wealth ratio to understand the paradox. Consider the table below where we have compared a static SIP with four different types of stepped-up SIPs with different levels of step up. The results may actually surprise you.

This may sound paradoxical. Why does my wealth ratio not go up when I step up? That is not much of a worry. The lower wealth ratio is more because higher SIPs are happening for a shorter time period. What really matters in stepped-up SIP is that it inculcates in you the discipline to increase your SIP investment in sync with your income.

-The Article has been authored by Mr.Sandeep Bhardwaj, Chief Sales Officer & it appeared on 19th February, 2019 on the following website -www.dnaindia.com

Published on: Mar 2, 2019, 6:00 PM IST

We're Live on WhatsApp! Join our channel for market insights & updates

Get the link to download the App