With the growing fraudulent activities in the financial sector of the country, it has become important to keep records of all the customers. To curb these illicit activities, the Government of India launched an initiative, Central Know Your Customer (CKYC). It helps the government to know the customer and to keep your investments secured. Earlier, separate institutions had different KYC formats. However, the introduction of CKYC will bring processes from different financial entities under one platform.

What is CKYC?

Central KYC or CKYC is a centralized repository that stores all the personal details of the customer. CKYC registry is managed by the Central Registry of Securitisation Asset Reconstruction and Securities Interest of India (CERSAI). With the launch of CKYC, the customer is not needed to go through the same process again while transacting with any other financial institution. Below-mentioned are the features of CKYC repository: ● Gives a unique 14-digit number that is linked the customer’s ID proof ● Electronically stores personal data of the customer ● Verifies submitted documents submitted with the issuer ● Informs all the concerned institutions in case of any change in the KYC details All the financial institutions registered under SEBI (Securities & Exchange Board of India), RBI (Reserve Bank of India), IRDAI (Insurance Regulatory and Development Authority of India) and PFRDA (Pension Fund Regulatory & Development Authority) have to mandatorily register their customers under CKYC. Once you have transacted for the first time with any of these financial institutions, they will register your KYC with the Central KYC registry.

How does it work?

If you are a potential investor, you need to undergo the CKYC process. When you approach any institution to invest, they will first ask you to complete your KYC and submit required documents. These documents will then be sent to CERSAI, who in turn will allocate you a unique 14-digit KYC number. After your CKYC number is generated, everytime you wish to invest in any other institution, you don’t have to go through the KYC process again. That institution will submit your KYC number and will request CERSAI to furnish your documents making investing hassle-free for you.

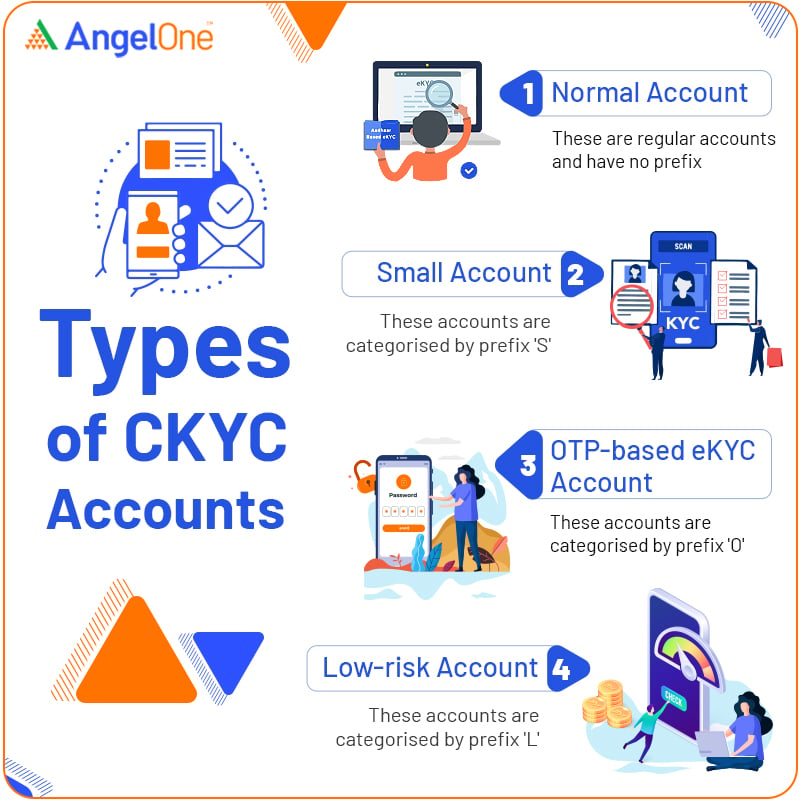

Types of CKYC accounts

Below are the types of CKYC accounts for individuals:

Below are the types of CKYC accounts for individuals:

-

Normal Account

When you submit any one of the below-mentioned documents, a Normal Account will be created.

- PAN

- Aadhar Card

- Driving License

- Voter ID

- Passport

- Mahatma Gandhi NREGA (National Rural Employment Guarantee Act) Job Card

-

Simplified/Low-risk Account

When you couldn’t submit any of the above-mentioned documents, you can submit other officially verified documents as specified by the RBI such as telephone bills (not more than 2 months old), electricity bills (not more than 2 months old), property tax receipts and bank account statements. In such a case, your account will be categorized as Simplified/Low-risk Account.

-

Small Account

If you don’t have officially valid documents, open a Small CKYC Account after submitting a filled-in form along with a photograph. However, these accounts will be subjected to restrictions in transactions and will have limited validity.

-

OTP-based eKYC Account

This account will be created when you submit an Aadhar-based PDF file that is downloaded from the UIDAI website and is enabled by an OTP.

Benefits of CKYC

From saving time to making investing easier, CKYC has multiple benefits. Following are a few of the benefits of CKYC: ● It saves time and energy as it unifies data from all the financial regulators and you won’t have to go through the entire documentation process again and again ● You have access to your CKYC details, enabling you to update your details in the CKYC registry anytime with ease ● Helps in controlling money laundering and other illegal activities in the financial sector ● Retrieving the investment data and related details have become easier for the authorities ● Same CKYC number can be used to enter into different financial transactions such as investing in the stock market, starting a mutual fund, opening a bank account, buying an insurance policy and more

How is it different from KYC and eKYC?

Below table will help you understand the difference between KYC, eKYC and CKYC

| Particulars | KYC | eKYC | CKYC |

| Allow Transactions With | Individual financial institution | Individual financial institution | All the companies registered under RBI, SEBI, IRDA and PFRDA |

| Documents Required | KYC form along with supporting documents | Aadhar Card | Duly filled CKYC form, ID proof, address proof and 1 photograph |

| Verification | In-person verification is done after documents are submitted | OTP or Biometric Verification - either of these 2 methods | CERSAI verifies documents submitted by you with the issuer |

Process of completing your CKYC registration When you transact with any of the financial institutions regulated by RBI, SEBI, IRDAI or PFRDA, they will register your KYC details with the CERSAI. Check your CKYC number online You can approach the financial institutions like your bank, stock broker and insurance company where you provided CKYC documents to know your CKYC number.

Conclusion

In the modern era, when we all want things to happen in a blink of an eye, this new process of CKYC is like a blessing in disguise. As with the introduction of Central KYC registration, transacting with financial institutions has become simpler, safer, and quicker. You can now transact with multiple financial entities without having to go through the same KYC process repeatedly making it easier and hassle-free for you.